Midterm Exam

Advanced Econometrics I, Fall 2016

代考高级计量经济学 The Gauss-Markov theorem states that under standard assumptions, the least squares estimator has the smallest variance among any other estimators.

Check the point for each question and do not spend too much time on any one question.

Question 1 (20)

True/False questions: please answer whether the following statements are true or false.No explanation is required, but you can add some clarification if you think you need.

a. (5) Consider a linear regression model: Yi = Bo + β1xi + Ei with all standard assumptions satisfied. Suppose that Ho : β1 = 0 is rejected at 10% significance level. It means that the 90% confidence interval of β1 does not contain 0. 代考高级计量经济学

b. (5) The Gauss-Markov theorem states that under standard assumptions, the least squares estimator has the smallest variance among any other estimators.

c. (5) Given any standard normal random variable and chi- squared random variable,we can always construct a t random variable.

d. (5) Consider a linear regression model under standard assumptions. When we estimate the parameters using the least squares method, the resulting residual always has a zero sample covariance with any independent variable of the model.

Question 2 (20) 代考高级计量经济学

A researcher studies the effect of the global carbon emission on climate change. Let xt be the total amount of carbon emission at time t measured in ‘toe (ton of oil equivalent)’,Yt be the average air temperature at t measured in Celsius. Assume that x and y are linearly related as in the following:

Yt= βo+ β1xt十∈t,

where∈t ~ i.i.d.N(0, σo2) satisfying all standard assumptions. Given data of {xt,yt}h=1, you can compute the estimates of the parameters,βo and β1.

a.(10) Now suppose that another researcher conducts the same study using another dataset ![]() where xt is the carbon emission measured in‘tCO2e (ton of CO2 equivalent’ and YI is the air temperature measured in Fahrenheit.1 She estimates the parameters: 阳and p1. Express。and β1 in terms of βo and β1. 代考高级计量经济学

where xt is the carbon emission measured in‘tCO2e (ton of CO2 equivalent’ and YI is the air temperature measured in Fahrenheit.1 She estimates the parameters: 阳and p1. Express。and β1 in terms of βo and β1. 代考高级计量经济学

b. (5) Now focus on the least squares estimator β1 in the original study. Note that β1 is a random variable. Briefy explain what it means. Write down the expression for the (conditional) variance of β1.

c. (5) In the second study, you want to compute the (conditional) variance of β*.Express it in terms of the original conditional variable (V ar(B1|X)). Is its numer-Express it in terms of the original conditional variable (V ar(B1|X)). Is its numer-study is less (more) precise than β1 in the original study?

1![]() where C and F are the temperature measured in Celsius and Fahrenheit, respectively.Also assume that 1 toe is equal to 3 tCO2e. By the way, this researcher must be American. :-p

where C and F are the temperature measured in Celsius and Fahrenheit, respectively.Also assume that 1 toe is equal to 3 tCO2e. By the way, this researcher must be American. :-p

Question 3 (10) 代考高级计量经济学

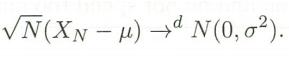

Assume that a random sequence XN satisfies the following condition (μ < 0):

a. (5) Find the asymptotic distribution of

b. (5) What is the asymptotic correlation cofficient between X元and -3XN + 1?What is the asymptotic correlation coefficient between exp(XN) and -3XN十1? (Hint: Asymptotic correlations are calculated from asymptotic variances and covariances.)

Questions 4 & 5 are ‘cumulative’ in that you need to have the answer of (a) to solve (b), (c) and so on. Even if you cannot obtain the answer of (a), still try your best and describe at least the formula for subsequent questions to get partial credits.

Question 4 (25)

Assume that all standard assumptions are satisfied. A multiple regression of y on a constant, x1 and x2 produces the following results:

![]()

From the data, you obtain the following information:

a. (5) Let the constant be Bo and the two slopes be (B1,B2)’. You want to know whether x1 has any significant effect on y. So, you test Ho: β1 = 0 and obtained the t-statistic of 2. What is the implied standard error of β1, s.e.(B1)? What is the implied estimate of the error variance, δ2?

b. (5) What is the number of observations? What is the implied residual sum of squares (RSS)?

Hint: Recall the meaning of each entry in X’X.

c. (5) Now you want to conduct the overall goodness-of-fit test. Express the null hypothesis in the form of Rβ = q, whereβ = (Bo, B1, B2)’. What are the expressions for R and q? What is the value of the F-statistic?2 Is the null rejected at the 5% significance level? 代考高级计量经济学

d. (5) The F-statistic for the overall goodness- of-fit test can be also obtained from the goodness-of- fit measure (R2), the number of observations (N) and the dimension of β (K). Use this relationship to find the implied R2.

2For simplicity, you can assume that

e. (5) W hat should be the total sum of squares (TSS)? What is the adjusted goodness-of ft (R2)?

Question 5 (25) 代考高级计量经济学

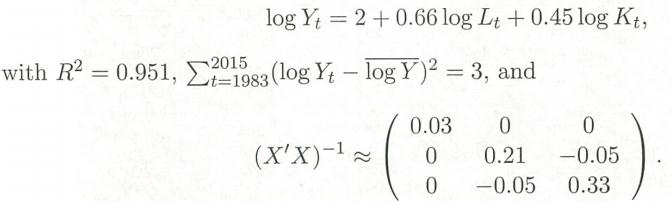

Consider the model under the standard assumptions:

![]()

where Yt is the real GDP, and Lt and Kt are total input of labor and capital, respectively. All variables are annually observed. Assume that Lt and Kt are exogenous (non-random)and∈t ~ i.i.d.N(0, σ2). The estimated equation is

a. (5) Explain the meaning of the estimated slope cofficients.

b. (5) Using the goodness of-fit measure and the total sum of squares, find the value of the residual sum of squares. Also answer what the implied σ2 is.

d. (5) Recall that we can test this joint null hypothesis using a diferent approach: unrestricted and restricted models. Given the unrestricted model (Equation (1)),write down the model restricted by the null hypothesis. 代考高级计量经济学

e. (5) What is the implied restricted residual sum of squares (RSSr)?

Hint: Use the fact that the two approaches should result in the same conclusion (same. F-statistic).

3[Aside] When β1 + β2 = 1, the production function is said to have constant returns to scale.

更多代写:java编程代写 考试助攻 Statistics统计学代写 Literature Review代写北美 Philosophy哲学论文代 r语言代做价格

合作平台:essay代写 论文代写 写手招聘 英国留学生代写