BU.232.620 (Linear Econometrics for Finance)

Homework 2

代写金融线性计量经济学 Suppose we only change the unit of yi to percentage points, i.e., the IBM stock return yi will be 5 for the 5% monthly return.

1.For the SLR model yi = 0 + 1xi + ui , with yi as the IBM stock return and xi as the market return (CAPM) that are both in original units, e.g., 0.05 means 5% monthly return. 代写金融线性计量经济学

- Suppose we only change the unit of xi to percentage points, i.e., the market return xi will be 5 for the 5% monthly return. Does this change the values of

β0 , and β1 ? If so, by how much?

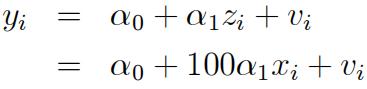

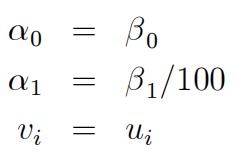

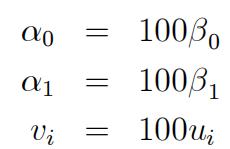

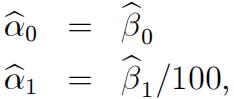

Answer: Changing the unit of ; to percentage points means we multiply x; byAnswer:100, with the new regressor defined as z; = 100.;. Let the new regression model be

Compare this regression equation to the original regression yi = , + i + ui,we have

Therefore. the value of 6, does not change, while that of , get divided by 100 代写金融线性计量经济学

- Suppose we only change the unit of yi to percentage points, i.e., the IBM stock return yi will be 5 for the 5% monthly return. Does this change the values of β0 ,and β1 ? If so, by how much? 代写金融线性计量经济学

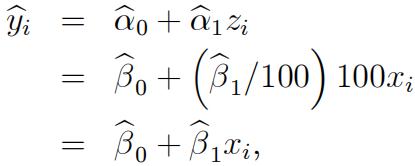

Answer:Changing the unit of yi to percentage points means we multiply yi by 100. with the new regressand defined as gi = 100y. Let the new regression model be

![]()

which is equal to

![]()

Compare this regression equation to the original regression yi = + Bi + ui,we have

Therefore, the values of both 6, and 6, get multiplied by 100.

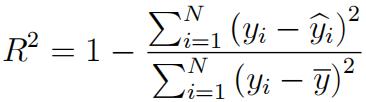

- Do the two changes of units above make R2different? Use the definition of R2to prove it.

Proof: We have by definition:

In the first case, i.e., changing the unit of x; to percentage points, we observe fromabove that neither y; or y changes. As a result the denominator does not changeIn the numerator, we just need to show y; does not change, which follows from 代写金融线性计量经济学

where we used

which follows from the sample counterpart of (2)In the second case, i.e.. changing the unit of y to percentage points, the denominator of R2is ![]() . Then we just need to show

. Then we just need to show ![]() gets multiplied by 100, which follows from the sample counterpart of (1).

gets multiplied by 100, which follows from the sample counterpart of (1).

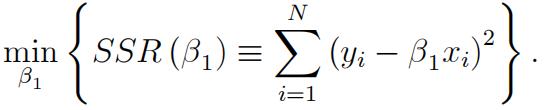

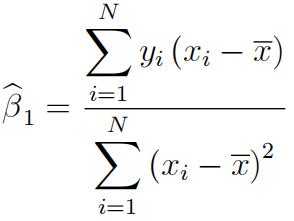

2.For the SLR model yi = 6x; + ui, i.e., regression without intercept,. 代写金融线性计量经济学

- Use the OLS principal to derive the OLS estimator of 6, for this model.

Answer: The OLS minimization problem is:

Taking the first order derivative, we have

Then the OLS estimator is

- Compare the OLS estimator for this regression with that for the regression withintercept. Under what conditions are the two estimators equal to each other?

Answer: From the OLS, we have the estimator for SLR as

Therefore, for β∼=β∼, we need x = 0.

更多代写:北美作业代写价格考 托福代考被抓 代写作业违法吗 apa格式要求 论文标准格式 如何写简历

合作平台:essay代写 论文代写 写手招聘 英国留学生代写