ST302

Stochastic Processes

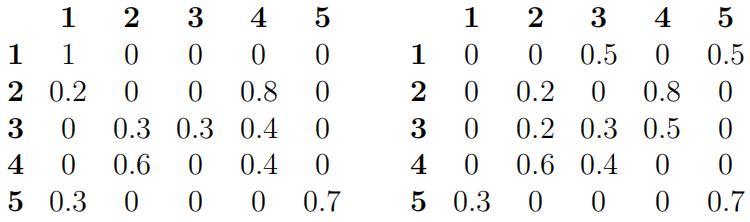

Stochastic Processes代考 Identify the transient and recurrent states, and the irreducible closed sets for the Markov chains with following transiton matrices.

Instructions to candidates

This paper contains 5 questions. Answer ALL questions.

Time allowed – Reading Time: None

Writing Time: 3 hours

You are supplied with: Murdoch & Barnes Statistical Tables, 4th edition

You may also use: No additional materials

Calculators: Calculators are not allowed in this examination

1. Identify the transient and recurrent states, and the irreducible closed sets for the Markov chains with following transiton matrices. [8 marks]

2.Consider a Markov chain (Xn)n≥0 with the countable state space {0, 1, 2, . . .} and the following transition probabilities:

p(i, i + 1) = p, i ≥ 0;

p(i, i − 1) = q, i ≥ 1;

p(i, i) = 1 − p − q, i ≥ 1,

p(0, 0) = 1 − p,

where p > 0 and q > 0. Let Vi := min{n ≥ 0 : Xn = i} be the fifirst time that the chain visits i. Stochastic Processes代考

a) Explain why this Markov chain is irreducible. Is it also aperiodic?Show your reasoning. [5 marks]

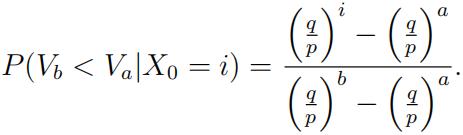

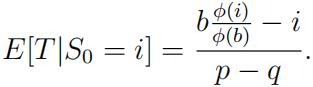

b) Let a, b and i belong to the state space of X such that a < i < b.Without using the Optional Stopping Theorem show that

[8 marks]

c) Assume p < q and show that the limiting distribution π is given by

[8 marks]

3.Let S be a random walk adapted to (Fn)n≥0 such that Stochastic Processes代考

P(Sn+1 = Sn + 1|Fn) = p,

P(Sn+1 = Sn − 1|Fn) = q, and

P(Sn+1 = Sn|Fn) = 1 − p − q,

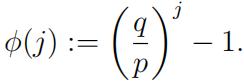

for some p > 0 and q > 0. Defifine

a) Show that φ(S) is a martingale with respect to (Fn)n≥0. [4 marks]

b) Defifine Mn = Sn − n(p − q) for n ≥ Show that M is martingale with respect to (Fn)n≥0. [4 marks]

c) Assume p≠q and let T = min{n ≥ 0 : Sn = b or Sn = 0}. Show that whenever 0 ≤ i ≤ b we have

[8 marks]

4.Let N be a Poisson process with intensity λ and adapted to some fifiltration (Ft)t≥0.

a) Show that Nt−λt and (Nt−λt) 2−λt are martingales with respect to (Ft)t≥0. [8 marks]

b) Consider the time of the n-th arrival Tn := inf{t ≥ 0 : Nt = n} and let m > n. Show that

[8 marks]

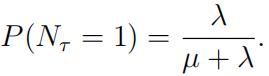

c) Suppose there exists another adapted Poisson process Z with in-tensity µ, which is independent of N. Let Xt = Zt +Nt and defifine τ := inf{t ≥ 0 : Xt = 1}. Show that

(Hint: Consider P(T1 < S1) where T1 and S1 are the fifirst arrivals for N and Z respectively and recall that the time of fifirst arrival for a Poisson process has exponential distribution.) [6 marks]

5.Let B denote a Brownian motion with B0 = 0. Stochastic Processes代考

a) State the defifinition of a Brownian motion. [4 marks]

b) Prove that exp![]() sin(Bt) and

sin(Bt) and ![]() exp

exp![]() can be written as stochastic integrals with respect to B. [6 marks]

can be written as stochastic integrals with respect to B. [6 marks]

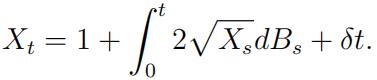

c) Let δ > 2 and consider X, which solves the following SDE:

Find a constant α for which ![]() can be written as a stochastic integral with respect to B. (Take that X never hits 0 for granted.)[5 marks]

can be written as a stochastic integral with respect to B. (Take that X never hits 0 for granted.)[5 marks]

d) Solve the following stochastic difffferential equation:

dYt = aYtdt + (b(t) + cYt)dBt ,

where Y0 = 0. (Hint: Try a solution of the form ZtHt where Zt = exp![]() and dHt = F(t)dt + G(t)dBt for some adapted process F and G which need to be determined.) [8 marks]

and dHt = F(t)dt + G(t)dBt for some adapted process F and G which need to be determined.) [8 marks]

e) It is well known that for any deterministic function f(t) the ran-dom variable ![]() is normally distributed. Find its mean and variance. [2 marks]

is normally distributed. Find its mean and variance. [2 marks]

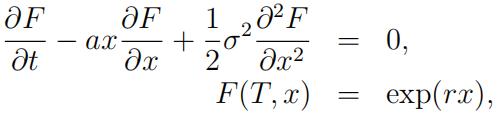

f) Use Feynman-Kac representation result to fifind a function F(t, x) that solves

where a, r and σ are real constants. You may want to use the fact that ![]() for any u ∈ R where Z is a standard Normalrandom variable. [8 marks]

for any u ∈ R where Z is a standard Normalrandom variable. [8 marks]

更多代写:HIS历史代写 雅思保分 education代写 1000字Essay代写 留学论文辅导 总结怎么写

合作平台:essay代写 论文代写 写手招聘 英国留学生代写