Mathematics and Statistics

ACSC/MATH 216

Final Exam (Version 2)

math数学代考 It is your responsibility to convince me that you know what you are doing. Clarity, completeness, and organization count.

| Problem | Total Possible Marks | Earned Marks |

| 1 | 20 | |

| 2 | 20 | |

| 3 | 20 | |

| 4 | 20 | |

| 5 | 20 | |

| Total | 100 |

Examination Directions math数学代考

1.If the last digit of your student id is either 0 or 1 or 3 or 4 or 7, thisis the correct version for

2.This exam is being held and proctored remotely through a live Zoom meeting. Sitand face an engaged camera to enable

3.There are 5 questions, with assigned marks as indicated, for a total of 100 points.

4.Nobooks or notes are allowed for this exam.

5.Non-programmable calculators including the following models of Texas Instru- ments calculators are permitted in the exams: BA-35, BA II Plus (Professional), TI-30Xa, TI-30X II and TI-30XS. Make sure that the memory has been cleared for TI-30X II and TI-30XS. Calculator instructions will not be permitted in the exams. math数学代考

6.Uploada single pdf file with scanned pages of all your answers no later than 11:15 am.

7.Pleaseshow all of your There will be partial marks available for each step of solution. It is your responsibility to convince me that you know what you are doing. Clarity, completeness, and organization count.

8.Round your answers for prices and rates to two and three decimal places, re- spectively.

9.Goodluck!

1.A 25 year annual coupon bond with face and redemption amount of 2000 is sellingat an e↵ective annual yield rate equal to twice of the annual coupon The present value of the redemption amount is equal to the present value of the coupons. math数学代考

(a)Determinethe purchase price of the bond at issuance.

(b)Determinethe amount for amortization of premium (or the principal repaid) in the 20th coupon.

(c)Suppose the bond was issued January 15, 2010, and is bought by a new purchaser on January 15, 2020 immediately after the coupon payment for a price of 1500. Find the internal rate of return earned by the original bondholder.

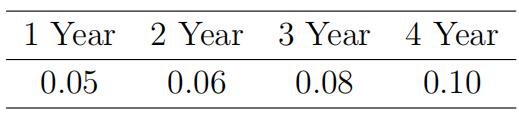

2.Attime 0, the term structure of e↵ective annual yield rates for zero coupon bonds is given as follows:

1- and 2-year maturity: 8%

3- and 4-year maturity: 10%

(a)Determine the price of a 4-year annual coupon bond with face amount 100 and coupon rate6%.

(b)You are given that the price of a 5-year annual coupon bond with face amount 100 and coupon rate 6% is 80. Determine the forward e↵ective annual interest rate for the period from time 4 to time 5,e., f [4, 5]. math数学代考

(c)A lender o↵ers to lend you 1000 for one year at rate 12% starting twoyear from now. Construct transactions that provide an arbitrage gain and give the amount of the gain.

3.Liability payments of 100 each are due to be paid in 2, 5 and 8 years from now. Asset cashflow consists of A3in 3 years and A6 in 6 years. The yield for all payments is 10%. An attempt is made to have the asset cash flow immunize the liability cashflow by matching present value and duration.

(a)Determine the Macaulay duration and the Macaulay convexity of the liabil- ity cashflow.

(b)Determine A3and A6.

(c)Determine whether or not the conditions for Redington immunization are satisfied.

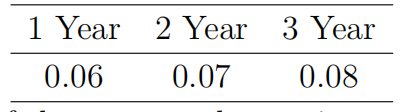

4.Theterm structure of (annual e↵ective) interest rates is as follows: math数学代考

Suppose that the notional amount of a 4-year interest rate swap of floating in- terest rate for fixed interest rate is 1,000 for the first year and 2,000 for the second and third years, and 4,000 for the fourth year.

(a)Find the swap rate.

(b)Atthe start of the second year, the term structure is

Find the market value of the swap to the receiver at the start of the second year.

5.A coupon bond has a spot price of The bond will pay coupons of 50 in6 months and in one year. The risk free rates are 9% (per year continuously compounded) for 6 month maturity and 10% for one year maturity.

(a)Find the delivery price for a one year forward contract on the bond, with deliveryimmediately after the coupon payment. math数学代考

(b)Suppose that immediately after the first coupon is paid, the continuously compound risk-free rate of interest is 10% for 6 month maturity, and thespot price of the bond has risen to Determine the value of the long position in the original forward contract entered at time 0.

更多代写:Math数学网课代考 多邻国代考 澳大利亚Cs网课代考 Personal Statement个人陈述代写 Political论文代写 学术抄袭

合作平台:essay代写 论文代写 写手招聘 英国留学生代写