Stochastic Foundation of Finance (FIN 538)

Finance金融代写 Problem 1 Consider a world with only two dates: today and tomorrow. There are two possible states tomorrow: Good and Bad.

Problem Set 6 Finance金融代写

(Please submit to Canvas by Friday, Oct 30 before midnight.)

Problem 1 Consider a world with only two dates: today and tomorrow. There are two possible states tomorrow: Good and Bad. There are two difffferent risky stocks A, B and no other assets in the market. Assume there is no arbitrage. The probability of the two states and the current prices and future (state-contingent) prices of the assets are listed below.

- Construct a portfolio of A and B in which the risk associated with A is exactly offffset by the

risk of B (that is, use B to hedge A). In other words, this portfolio is risk free.

- Compute the risk-free rate in the market.

- Does the risk-free rate depend on the prospect of the economy (that is, the probabilities of Good and Bad states)? Explain why or why not.

Problem 2 Finance金融代写

Consider the price of a security that follows the process in the fifigure below. At each time t = 0, t = 1, the price jumps up or down with a (physical) probability![]()

1.Are investors who trade this security risk-averse, risk-neutral or risk-loving?

2.Find the probability q (of the price going up) at which investors can price the security as if they’re risk neutral.

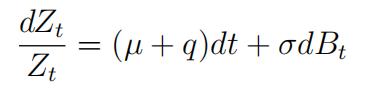

Problem 3 In this problem you will extend the Black-Scholes formula to a stock that pays a continuous dividend. Assume a stock pays a dividend at a constant yield of q and the dividends are being reinvested in the stock.

- Show that if the stock price follows a GBM of the form

then the value of a portfolio Zt in which an investor starts with one share at t = 0 and all dividends are reinvested follows a GBM of the form

(1)

Hint. Since Zt is the value of the portfolio at time t, the number of shares at time t is ![]() Therefore, at time t + dt, the value of the portfolio is

Therefore, at time t + dt, the value of the portfolio is

where the second term is the dividend paid out at t + dt. Use this expression and Ito’s rules(dt ∗ dt = 0, dBtdt = 0) to show (1).

2..Use Ito’s Lemma, verify that any Zt = ceqtSt , where c ≠ 0 is a constant, satisfifies (1) bycomputing  Since Z0 = S0, conclude that c = 1. Finance金融代写

Since Z0 = S0, conclude that c = 1. Finance金融代写

3.Now consider the same exercise only that you start at t = 0 with e−qT shares. Let the value of this portfolio at time t be ZtT . Show that ZtT still follows the stochastic process (1), but ![]() . Conclude that

. Conclude that  .

.

4.Conclude that a European call option with strike price K on ZtT follows exactly the same partial difffferential equation and the same terminal condition as the original B-S equation without dividends (note: the drift of the process of ZtT is difffferent from that of St , but it does not affffect the difffferential equation since the drift does not appear in the difffferential equation).

5.Show that the value of a European call option on Zt at time t is given by

where

更多代写:math网课代做 雅思网考 fin作业代写 Goal Essay代写 java论文代写 代写国外毕业论文

合作平台:essay代写 论文代写 写手招聘 英国留学生代写