Econ 7780

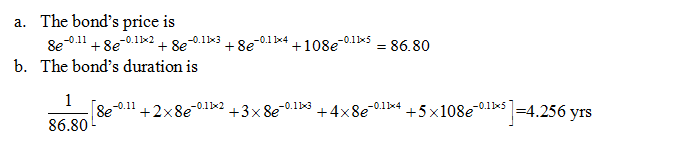

Economics代写 A five-year bond with a yield of 11% (continuously compounded) pays an 8%coupon at the end of each year.(a) What is the bond’s price?(b)···

Q9.7 Economics代写

A five-year bond with a yield of 11% (continuously compounded) pays an 8%

coupon at the end of each year.

(a) What is the bond’s price?

(b) What is the bond’s duration?

(c) Use the duration to calculate the effect on the bond’s price of a 0.2% decrease

in its yield.

(d) Recalculate the bond’s price on the basis of a 10.8% per annum yield and verify

that the result is in agreement with your answer to (c).

c.According to the notation in the chapter Economics代写

![]()

the effect on the bond’s price of a 0.2% decrease in its yield is

86.80*4.256*0.002=0.74

86.80+0.74=87.54

So the bond’s price should increase from 86.80 to 87.54.

Q 9.11

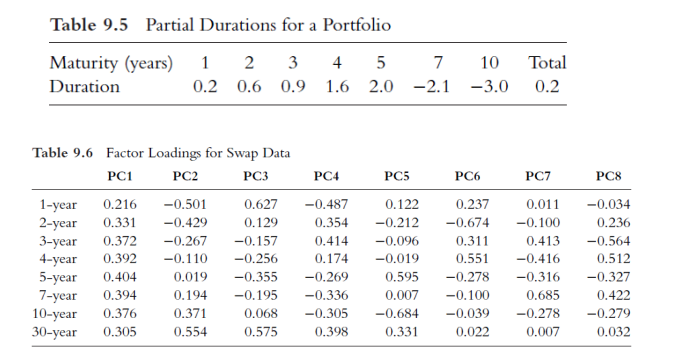

Consider a $1 million portfolio with the partial durations in Table 9.5. Estimate delta with respect to the first two factors in Table 9.6.

The delta with respect to the first factor (PC1) is -20*0.216-60*0.331-90*0.372-160*0.392-200*0.404+210*0.394+300*0.376=-5.64

The delta for second factor (pc2) is, Economics代写

-20*(-0.501)-60*(-0.429)-90*(-0.267)-160*(-0.11)-200*0.019+210*0.194+300*0.371=225.63

Thus, the delta to the two factors are -5.64 and 225.63 respectively.

Q9.17

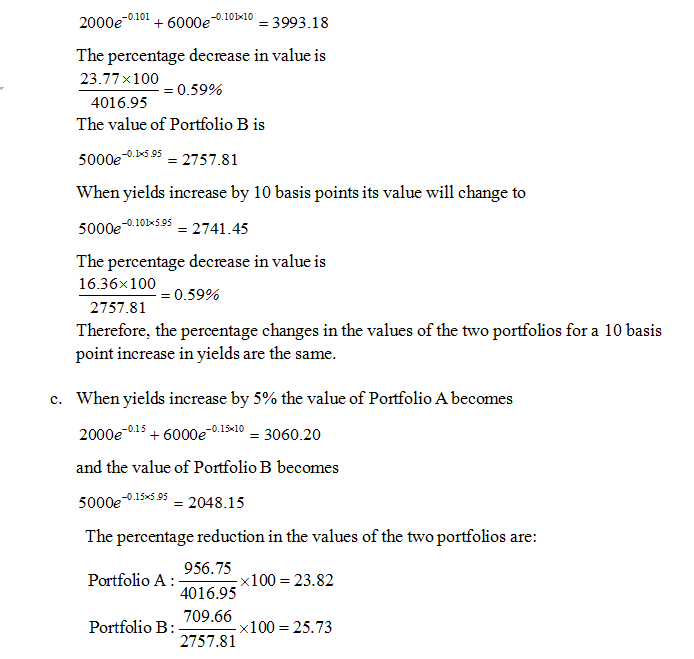

Portfolio A consists of a one-year zero-coupon bond with a face value of $2,000and a 10-year zero-coupon bond with a face value of $6,000. Portfolio B consists of a 5.95-year zero-coupon bond with a face value of $5,000. The current yield on all bonds is 10% per annum (continuously compounded).

(a) Show that both portfolios have the same duration.

(b) Show that the percentage changes in the values of the two portfolios for a 0.1%

per annum increase in yields are the same.

(c) What are the percentage changes in the values of the two portfolios for a 5%

per annum increase in yields?

a.The duration for Portfolio A is Economics代写

Since this is also the duration of Portfolio B, the two portfolios do have the same duration.

b.The value of Portfolio A is

![]()

When yields increase by 10 basis points its value will change to

Because the percentage decline in value of Portfolio A is less than that of Portfolio B, Portfolio A has a greater convexity.

Q9.18

What are the convexities of the portfolios in Problem 9.17? To what extent do (a) duration and (b) convexity explain the difference between the percentage changes calculated in part (c) of Problem 9.17?

For Portfolio A the convexity is: Economics代写

Following the same steps, for portfolio B the convexity is 5.952 or 35.4025. The percentage change in the two portfolios predicted by the duration measure is the same and equal to −5.95×0.05 = −0.2975 or –29.75%. However, the convexity measure predicts that the percentage change in the first portfolio will be

−5.95 × 0.05 + 0.5 × 55.40 × 0.052 = −0.228

and that for the second portfolio it will be

−5.95 × 0.05 = 0.5 × 35.4025 × 0.052 = −0.253

Duration does not explain the difference between the percentage changes. Convexity explains part of the difference. 5% is such a big shift in the yield curve that even the use of the convexity relationship does not give accurate results. Better results would be obtained if a measure involving the third partial derivative with respect to a parallel shift, as well as the first and second, was considered.

更多其他:代写作业 数学代写 物理代写 生物学代写 程序编程代写 Visualising Data代写