Stochastic Foundation of Finance (FIN 538) Master of Finance Program

Fall 2020 Sample Exam (Duration: 120 min)

金融Final exam代考 Using Ito’s lemma, compute the following Ito integral (that is,give it an expression in term of some Riemann integral over time

Question 1 (20 points in total): 金融Final exam代考

1a. (10 points) Let Xt be a stochastic process

dXt = eXt dt + log (Xt)dBt; t ∈ [0, T ]

where Bt is a Brownian motion. Using Ito’s lemma, compute the following Ito integral (that is,give it an expression in term of some Riemann integral over time, plus some elementary functions of processes X and B)

1b. (10 points) Suppose that the process Xt = eat+Bt is a martingale. Find a and calculate E[Xt|Fs], s < t for that value of a.

Question 2 (30 points in total): 金融Final exam代考

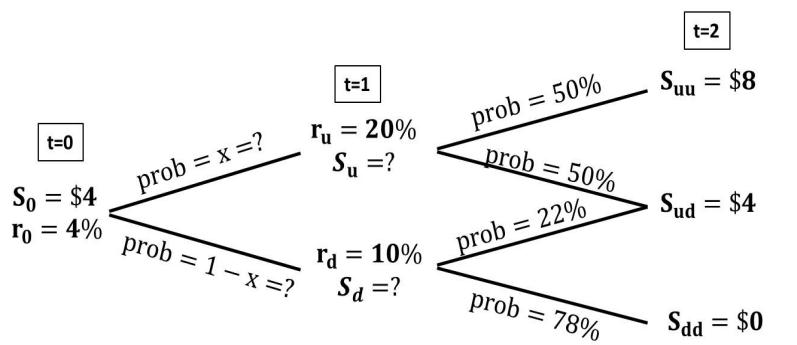

Let’s consider a world with three dates t = 0, 1, 2. Refer to the graph below. Consider a stock that pays nothing at t = 1, and st t = 2 pays: Suu = $8 (if state at t = 2 is uu); Sud = $4 (if state at t = 2 is ud); Sdd = $0 (if state at t = 2 is dd). The price at t = 0 of this stock is S0 = $4. The risk-free rate from t = 0 to t = 1 is r0 = 4%. If state at t = 1 is u, the risk-free rate will be ru = 20%. If state at t = 1 is d, the risk-free rate will be rd = 10%. The risk neutral probabilities are given the graph for the corresponding transitions.

2a. (10 points) Compute the value Su and Sd of this stock at t = 1

2c. (10 points) Compute the risk-neutral probability x for the transition from t = 0 to state u at t = 1.

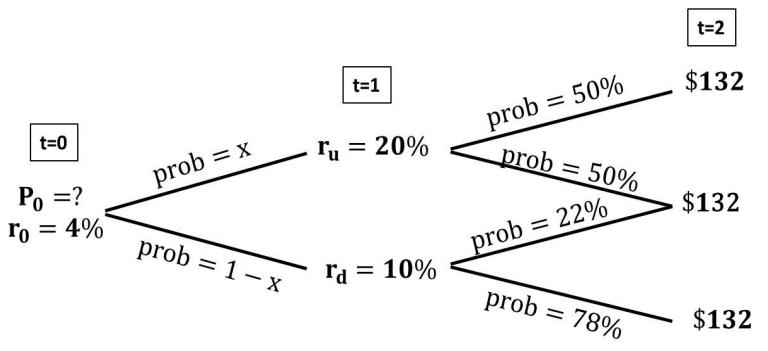

2d. (10 points) In the same market, compute the current (at t = 0) price P0 of a zero-coupon bond of face value of $132 (that is, bond pays nothing at t = 1, and pays $132 in any state at t = 2).

Question 3 (40 points in total): Consider a risky firm whose pre-tax value follows the stochas- tic process 金融Final exam代考

Vt = V0e0.5t+Bt

where Bt is a Brownian process. Let’s define effective tax τt such that, at any time t, one dollar of pre-tax value corresponds to (1 − τt) dollars of after-tax to the firm owner. Let’s assume that the effective tax is random and follows the process

τ = 1 − e(µ− 1 σ2)t+σBt

3a. (10 points) Express after-tax value St of the firm at time t in term of pre-tax value Vt and effective tax τt.

3b. (10 points) Using Ito’s lemma, express dVt, and dτt in terms of dt and dBt. 3c. (10 points) Compute the after-tax expected return rate of the firm at time t.

3d. (10 points) Compute the after-tax conditional volatility of the firm at time t. Give economic explanation for all terms in this conditional volatility.

Question 4 (10 points). Calculate V ar(∫ t s2dB ).

更多代写:新公共管理理论代写 GMAT代考 经济学网课代上价格 经济学留学生论文代写 金融?Finance Essay代写 essay标题

合作平台:essay代写 论文代写 写手招聘 英国留学生代写