CCDS 436 – [email protected]

金融assignment代做 InsTRUCTIONS: Do not discuss these problems with anyone or use any online resources for help until you have turned in your exam.

MA577 – MATHEMATICS OF F INANCIAL DERIVATIVES, FALL 2023

Final exam

InsTRUCTIONS: Do not discuss these problems with anyone or use any online resources for help until you have turned in your exam. You may use your textbooks and any class notes that you took. Make sure that you explain your reasoning clearly and justify where your answers come from. If you use a variable that is not defined in the problem, you must explain what the variable represents. Cheating and plagiarism will not be tolerated at all. Good luck!

NOTATION: For a standard normal random variable N ∼ N (0, 1), we denote by Φ(x) its distribution function,which is given by

PROBLEM 1- 35%

A European binary call option with strike K and maturity T on a stock S is an option that pays $1 at maturity if ST is strictly above the strike K and nothing otherwise. Similarly, a European binary put option with strike K and maturity T on a stock S is an option that pays $1 at maturity if ST is not above the strike K and nothing otherwise.

(5%)1.We denote by Bt + and Bt − the prices at time 0 ≤ t ≤ T of the binary call and the binary put, respectively.

What are the payoffs BT + and BT − of these binary options at maturity? 金融assignment代做

(10%)2.We assume that the risk-free rate is r > 0 (expressed with continuous compounding).

Assuming that the market is arbitrage-free, prove that for any time t ≤ T, the following binary call-put parity formula holds:

![]() (⋆)

(⋆)

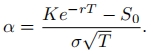

3.We now assume that the evolution of St is modeled by St = ert (S0 + σWt), where {Wt : t ≥ 0} is a standard Brownian motion. Let

(10%)(a) Prove that the price at time 0 of the above binary call option in this model is B0 + = e −rT (1 − Φ(α)). Is the call put parity relation (⋆) satisfied at time 0 in this model?

(10%)(b) Compute the deltas at time 0 of these binary call and put.

PROBLEM 2-10% 金融assignment代做

A $100 million interest rate swap has a remaining life of 10 months. Under the terms of the swap, 6-month LIBOR is exchanged for 7% per annum (compounded semiannually). The average of the bid-offer rate being exchanged for 6-month LIBOR in swaps of all maturities is currently 5% per annum with continuous compounding. The 6-month LIBOR rate was 4.6% per annum 2 months ago. What is the current value of the swap to the party paying floating?

PROBLEM 3- 35%

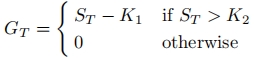

A European gap call option with strike K1, trigger K2 and maturity T on a stock S is an option of call type presenting a gap between the strike K1 (which determines the amount of the payoff in case the option is exercised) and the trigger K2 (which determines if the option is exercised or not). The payoff GT of the gap call is hence given by

We assume throughout this problem that K2 ≥ K1 (so that the payoff is always non-negative).G0 denotes the price at time 0 of the gap call option described above. Note that if K1 = K2, the gap call option is just a standard(vanilla) call option. 金融assignment代做

(5%)1.We denote by C0(K1) and C0(K2) the prices at time 0 of the standard (vanilla) call options with the same maturity T on the same underlying stock S with strikes K1 and K2, respectively. By an absence of arbitrage argument, establish an inequality between G0 and C0(K1) and another one between G0 and C0(K2).

(12%)2.In this question, we assume that the evolution of the stock price S is modeled by a binomial model with u = 1.1,d = 0.9 and δt = 3 months. Let the risk-free rate be r = 1% (expressed with continuous compounding) andS0 = 50.

Compute the price at time 0 of a gap call option with T = 6 months, K1 = 50 and K2 = 55.

3.In this question, we now assume that the evolution of St is modeled by the Black-Scholes model with a risk-free rate of r > 0 and a volatility σ > 0.

(8%)(a) Show that the payoff GT of the gap call option can be expressed as a linear combination of the payoff CT (K2) of the vanilla call option with strike K2 and the payoff 1{ST >K2} of a binary call option with strike K2.

(10%)(b) Prove that the Black-Scholes formula for the price G0 of a gap call is

PROBLEM 4-20% 金融assignment代做

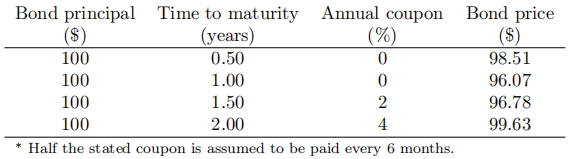

The following table gives the prices of treasury bonds (note that the annual coupon of each bond is given as a percentage, not a cash amount):

(5%)1.Find the 1.5-year zero coupon rate (continuously compounded).

(5%)2.What are the forward rates for the following periods: 6 months to 12 months, and 12 months to 18 months?

(10%)3.Use long and short positions in the above bonds to build a bond portfolio that is equivalent to a 1.5-year zero coupon bond with a principal of $10, 100.

更多代写:考试重考代考 gre代考被抓 金融学代修代写 留学生Essay Final代考 金融论文代写英国 代写密码学作业

合作平台:essay代写 论文代写 写手招聘 英国留学生代写