Paper Code: ACFI 342

MOCK PAPER

Financial Risk Management

金融风险管理代写 Using appropriate models, discuss the three factors that affect changes in the net worth of a financial institution when interest rates change.

INSTRUCTIONS TO CANDIDATES

Student declaration:

I confirm that I have read and understood the University’s Academic Integrity policy. I confirm that I have acted honestly, ethically and professionally in conduct leading to assessment for the programme of study. I confirm that I have not copied material from another source nor committed plagiarism nor fabricated data when completing the attached piece of work. I confirm that I have not previously presented the work or part thereof for assessment for another University of Liverpool module. 金融风险管理代写

I confirm that I have not colluded with any other student in the preparation and production of this work. I confirm that I have not incorporated into this assignment material that has been submitted by me or any other person in support of a successful application for a degree of this or any other University or degree awarding body. Students who require sympathetic marking should ensure that they attach the Sympathetic Marking Indicator to the first page of the document prior to submission

PLEASE ANSWER ALL QUESTIONS

QUESTION 1

a)Consider the coefficients of Altman’s Z-score. Comment on the size of the coefficients and explain which ratios appear to be the most important in assessing the creditworthiness of a loan applicant. Also, comment upon the key limitation of this method.[8 marks]

b)ABC Bank has the following balancesheet:

Suppose interest rates rise such that the average yield on rate sensitive assets increases by 45 basis points and the average yield on rate sensitive liabilities increases by 35 basis points.

Required 金融风险管理代写

(i)Calculate the repricing gap for ABC Bank

(ii)Assuming the bank does not change the composition of its balance sheet, calculate the net interest income for the bank before and after the interest rate changes. What is the resulting change in net interestincome?[10 marks]

(c)A.U.S. bank is raising all of its $20 million liabilities in dollars (one-year CDs) but investing 50 percent in U.S. dollar assets (one-year maturity loans) and 50 percent in U.K. pound sterling assets (one-year maturity loans). Suppose the promised one-year U.S. CD rate is 9 percent, to be paid in dollars at the end of the year, and that one-year, credit risk-free loans in the United States are yielding only 10 percent. Credit risk-free one-year loans are yielding 16 percent in the United Kingdom. What amount, in sterling, will the bank have to repatriate back to the U.S. after one year if the exchange rate remains constant at £1/$1.60?[10 marks] 金融风险管理代写

(d)Using appropriate models, discuss the three factors that affect changes in the net worth of a financial institution when interest rates change. Assume that only duration is used for portfolio immunization method.[10 marks]

(e)ABC Bank has the following balance sheet (in millions), with the risk weights in parentheses.

| Assets | Liabilities and Equity | ||

| Cash (0%) | $21 | Deposits | $176 |

| OECD interbank deposits (20%) | 25 | Subordinated debt (5 years) | 2 |

| Mortgage loans (50%) | 70 | Cumulative preferred stock | 2 |

| Consumer loans (100%) | 70 | Equity | 5 |

| Reserve for loan losses | (1) | ||

| Total Assets | $185 | Total liabilities and equity | $185 |

The cumulative preferred stock is qualifying and perpetual. In addition,

the bank has $30 million in performance-related standby letters of credit (SLCs) to a BBB-rated corporation,$40 million in two-year forward FX contracts that are currently in the money by $1 million, and $300 million in six-year interest rate swaps that are currently out of the money by $2 million. The counterparty of the derivatives contracts is also BBB-rated. 金融风险管理代写

| Credit conversion factors follow: | |

| Performance-related standby LCs | 50% |

| 1- to 5-year foreign exchange contracts | 5% |

| 1- to 5-year interest rate swaps | 0.5% |

| 5- to 10-year interest rate swaps | 1.5% |

Required

- What are the risk-adjusted on-balance-sheet assets of the bank as defined under the BaselAccord?

- Disregarding any capital conservation buffer, what are the core Tier I capital, the total Tier I capital, and the total capital required for both off- and on-balance-sheetassets?[12 marks]

QUESTION 2 金融风险管理代写

a)Discuss the JP Morgan RiskMetrics Model for measuring market risk and explain how it can be applied for FX, equity and bond portfolios.[14 marks]

b)John Orange, Vice President of operations of ABC Bank, is estimating the aggregate DEAR of the bank’s portfolio of assets consisting of loans (L), foreign currencies (FX), and common stock (EQ). The individual DEARs are £25,310, £23,155, and £67,328 respectively. If the correlationcoefficients ρij between L and FX, L and EQ, and FX and EQ are -0.2, 0.5, and 0.8, respectively, what is the DEAR of the aggregate portfolio?[12 marks] 金融风险管理代写

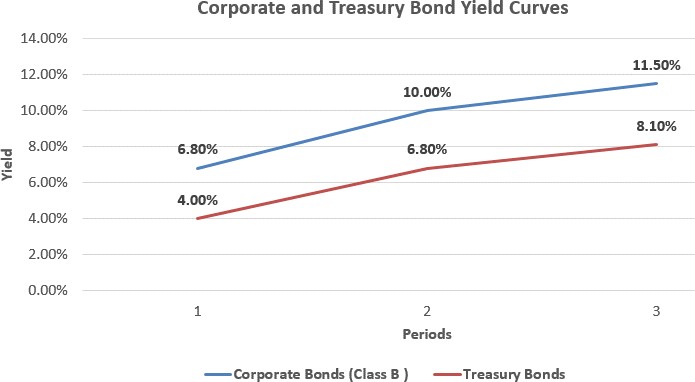

c)Calculate the term structure of default probabilities over three years using the following spot rates from the Treasury and corporate bond (pure discount) yield curves. Be sure to calculate both the annual marginal and the cumulative default probabilities.[16 marks]

(d)What are the two reasons that liquidity risk arises? How does liquidity risk arising from the liabilityside of the balance sheet differ from liquidity risk arising from the asset side of the balance sheet?[8 marks]

更多代写:cs代做靠谱吗 多邻国保分 Econ英国代考 compare essay代写 Course paper 代写 aje润色

合作平台:essay代写 论文代写 写手招聘 英国留学生代写