Pharmaceutical Industry analysis

英文report A biomedical pipeline takes about 5 to 10 years from phase preclinical research to MAA(Marketing Authorization Application).

Pharmaceutical Industry introduction 英文report

The United States has always dominated the pharmaceutical industry globally and achieved its industrialization. The biomedicine industry drives has become one of the core driving forces for the development of high-tech industries in the United States. The biopharmaceutical industry is a new type of technology-intensive industry in the United States and a pillar industry in the economic development of the United States.It has a significant influence. As the center of global biomedical development, five major biomedical industrial bases have been formed in Boston, San Diego, San Francisco, Washington, and the North Carolina Triangle Park. The US biomedical industry is booming, with about half of biomedical companies and half of biomedical patents in the world, and pharmaceutical sales account for more than 30% of the global biomedical product market.

An important feature of the biopharmaceutical industry is the long profit period. A biomedical pipeline takes about 5 to 10 years from phase preclinical research to MAA(Marketing Authorization Application). Therefore, in the research and development early stage, Biopharmaceutical company usually takes a long period (average 10 years) to reach the breakeven point and make a profit. At the beginning of Research & development phase, pharmaceutical companies demand a large amount of capital investment into R&D (exceeds 20% of sales revenue ) and do not generate some profits.

Therefore, in the early stages of the company’s establishment, pharmaceutical companies need more venture capital and market support.

As the company’s products mature and even the expiration of its patents, the company’s growth will be greatly reduced. The average life span of a relatively successful biopharmaceutical company in the United States is 4 years, and the average life span from listing to profitability is about 7 years. After generate profits, companies will undergo non-linear growth. Although governments worldwide control the increase of drug costs, the growth of the drug market is still faster than the rate of economic growth due to the development of new drugs, changes in the population structure, and people’s high expectations of health. It is predicted that CAGR of the entire pharmaceutical industry will continue to rise. 英文report

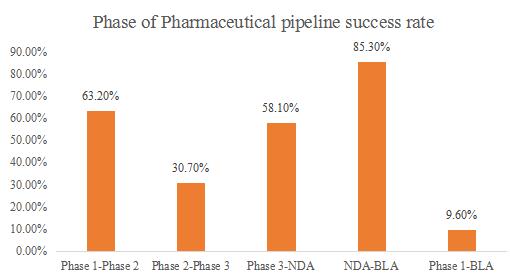

The annual R & D expense ratio of US pharmaceutical companies is very high. According to the various phases of drug development, the phases can be divided into several stages, including pre-clinical drug discovery, new drug clinical application, clinical trial (Phase I, Phase II, and III), NDA(new drug application), BLA(biologic License Application)and MAA(Marketing Authorization Application).Although the pharmaceutical companies face the difficulties, such as hard, long cycle time of new drugs development and the low clinical successful rate each phase, a increasing number of companies invest more capitals to Research & Development pipeline. The number of pipelines are blooming and the successful development of innovative drugs will generate more profits for the companies.

Source: Clinical development success rate 2005-2018

*NDA-New Drug Application/BLA-Biologic License Application

Source: Annual Reports from pharmaceutical companies

Global pharmaceutical industry competition 英文report

At present, global biopharmaceutical industry gradually form the pattern of cluster, which mainly concentrated in the United States, Europe, Japan, India, Singapore, China and other countries and regions. Among them, the United States, Europe, Japan and other developed countries and regions dominated the biopharmaceutical markets. The American biopharmaceutical industry’s R & D strength and industrial development are leading the world. For example, biopharmaceuticals have been widely used in the treatment of cancer, diabetes, and chronic diseases. In Europe, the solid industrial foundation and technological advantages foster the growth of the biopharmaceutical industry, which becomes the forefront of the world after following the United States.

Meanwhile, the increasing trend of the aging population has brought a broad market prospect in Europe. Although the development of Japan’s biomedical industry emerged later than European and American countries, it has developed very rapidly in the past few decades and has gained a leading position in Asia. The United States, the European Union, Japan and other developed countries hold more than 94% of patents, especially the United States holds nearly 60% of the world’s biopharmaceutical patents. 英文report

In terms of the valuation of the US pharmaceutical sector, the market value range of traditional pharmaceutical giants such as Pfizer, Novartis, Bristol-Myers Squibb and other pharmaceutical companies value 500 ~ 100 billion US dollars, the average growth rate of these companies’ net profit is less than 10%, and the PE (TTM) range is between 20 ~ 30. In addition, some medium-sized biotechnology companies, with a market value range of between $ 10 billion and $ 50 billion, have high valuations.

Most companies are driven by several durable core products, and net profit growth achieve rapid growth. The range of PE (TTM) is between 30 and 50.What’s more, the PE (TTM) range of generic drug companies is between 10-20. At present, it is worth noting that some new pharmaceutical and biotechnology companies in the U.S. pharmaceutical sector have higher investment in research and development, which the clinical pipelines are new drugs or therapies. Although the company has not yet generated profits or revenue, the market value close to tens or even tens of billions of dollars.

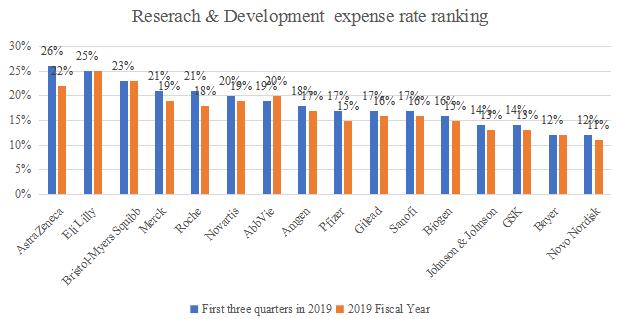

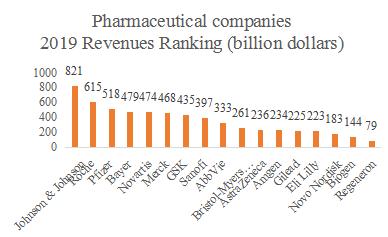

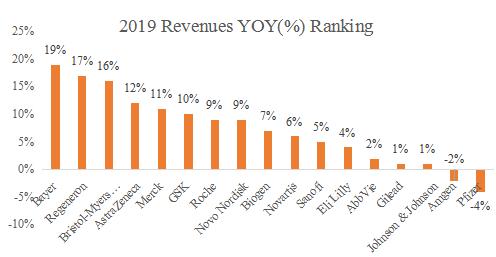

In terms of revenue growth, the average growth rate of 17 core pharmaceutical companies in 2019 was 6.1%. Regarding R & D expenses, the average R & D expense rate of 17 core pharmaceutical companies in 2019 is 20%, and high R & D investment is still the core driven factor for the long-term steady growth of multinational pharmaceutical companies. In the future, many companies will focus on the Chinese market.

With the aging of older population, the increase in per capita medical consumption and the promotion of various national policies in China, many overseas pharmaceutical companies will develop their business on the Chinese market where has a high demand for the various medicines. Meanwhile, based on the support of policy in China, many titan pharmaceutical companies in China achieve outstanding financial performance, and they will focus on developing the Chinese market in the future.

Source: Annual Reports from pharmaceutical companies

Source: Annual Reports from pharmaceutical companies

Pharmaceutical industry strategy analysis

| Elements | Explanation |

| Main Companies | Pfizer, Novartis, Merck, GlaxoSmithKline (GSK), Gilead |

| Barriers to Entry | High

• Effective competition requires significant financial and intellectual capital • A potential new entrant will be demand to create a sizeable R & D department, global distribution network, and large-scale manufacturing capabilities |

Concentration |

Concentration

A small number of companies occupy the global market for most branded drugs. Recent Mergers & Acquisitions have increased concentration |

| Impact of industry capacity | Less impact: The price of pharmaceuticals is mainly determined by patent protection and regulatory issues, including government or FDA approval of pharmaceuticals and manufacturing facilities. Less impact on manufacturing capacity 英文report |

| Industry stability | Stability: The branded drug market is dominated by major companies and consolidated through Mergers & Acquisitions. However, when new drugs are approved and accepted or patents are expired and lose production, market share will change rapidly. |

Life cycle |

Maturity: Overall demand remains steady each year |

| Price Competition | Low / Medium: Government and FDA take cost containment measures in healthcare systems in the United States, including the price control and lower price pressure. In a single payer system, the threshold of effectiveness is higher as prices account for a larger part of the decision-making process. |

| Demographic impact | Positive: The aging of older population in developed markets will increase slightly the demand of drugs |

| The government and regulatory impact | High: All drugs must be approved by FDA or national security regulations. The patent system varies from country to country.In addition, health care is highly regulated in most countries. |

| Social impact | None |

| Technology Impact | Medium / High: Bio (macromolecule) drugs are promoting new therapeutic field, and many large drug companies have a relatively small share of biotechnology |

| Industry characteristics :Growth VS Defense VS Cycle | Defense: Demand for most healthcare services will not fluctuate with the economic cycle, and the intensity of demand may not be considered “growth” |

Table: Bio-pharmaceutical industry strategy analysis framework

Market segment 英文report

Anti-viral market introduction

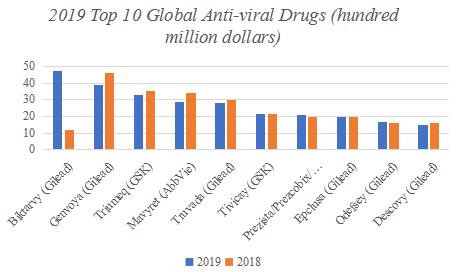

There are many industry segments in pharmaceutical Industry, including recombinant protein, cell therapy, monoclonal antibody drugs, antiviral industries and so on. Gilead mainly focuses on research in the field of anti-viral drugs, mainly concentrating on AIDS, liver disease, hematology/Oncology and other fields. According to Grand View Research data, the global antiviral drug market size will reach USD 56.4 billion in 2019, with a four-year CAGR of 8.23%. Among them, the total market size of the global antiviral drug TOP 10 reached 27 billion U.S. dollars, accounting for about half of the entire antiviral market size. In terms of the drug category, there are 8 anti-HIV drugs and 2 HCV drugs.

| Rank | Drugs | Company | Indication | 2018 | 2019 | YOY(%) | Rank in 2018 |

| 1 | Biktarvy | Gilead | HIV-1 infection | 11.84 | 47.38 | 300.20% | Genvoya |

| 2 | Genvoya | Gilead | HIV-1 infection | 46.24 | 39.31 | -15.00% | Triumeq |

| 3 | Triumeq | GSK | HIV-1 infection | 35.2 | 32.9 | -4.00% | Mavyret |

| 4 | Mavyret | AbbVie | HCV | 34.38 | 28.93 | -15.90% | Truvada |

| 5 | Truvada | Gilead | HIV-1 infection | 29.97 | 28.13 | -6.10% | Tivicay |

| 6 | Tivicay | GSK | HIV | 21.8 | 21.4 | 1.00% | Epclusa |

| 7 | Prezista/Prezcobix/Rezolsta | Johnson & Johnson | HIV-1 infection | 19.55 | 21.1 | 8.00% | Prezista/Prezcobix/Rezolsta |

| 8 | Epclusa | Gilead | HCV | 19.66 | 19.56 | -0.50% | Odefsey |

| 9 | Odefsey | Gilead | HIV-1 infection | 15.98 | 16.55 | 3.60% | Descovy |

| 10 | Descovy | Gilead | HIV-1 infection | 15.81 | 15 | 5.10% | Harvoni |

Table: 2019 Top 10 Global Anti-viral Drugs (hundred million dollars)

Graph:2019 Top 10 Global Anti-viral Drugs (hundred million dollars)

Anti-HIV segment market

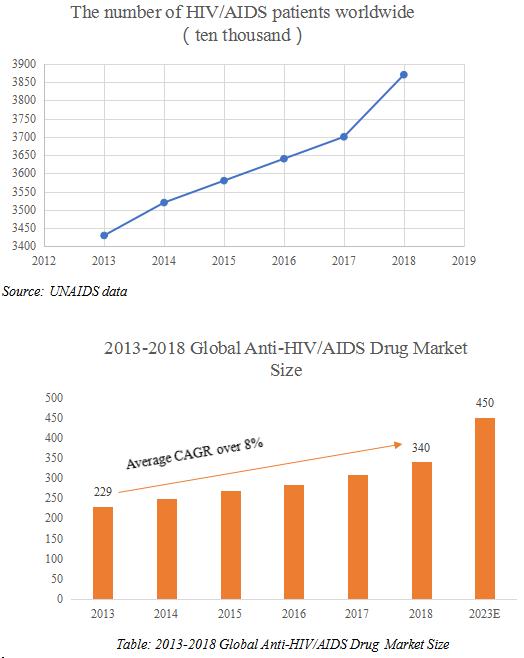

According to UNAIDS data, the number of HIV carriers and AIDS patients (HIV / AIDS) worldwide increased from 34.3 million at the end of 2013 to 37.3 million at the end of 2018, and the number of carriers is still increasing gradually year by year, indicating that there are a large market space and the market is not saturated yet.

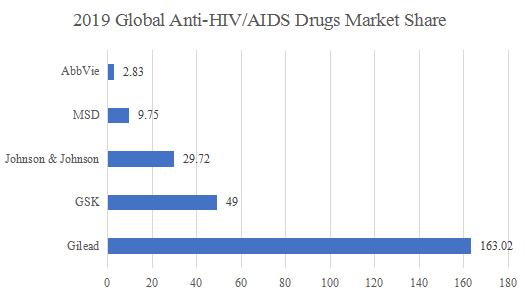

The global anti-HIV drug market size has rose from 22.9 billion in 2013 to 34 billion in 2018, with CAGR of more than 8%. It is expected that the global anti-HIV virus market will exceed $ 45 billion in 2023. At present, The global anti-HIV virus drug market has formed an oligopoly pattern with a high concentration. In particular, Gilead, an flagship company in the antiviral field, has focused on the development of antiviral drugs, making Gilead dominate the HIV market segment. In the global Anti-HIV drug market, Gilead, GlaxoSmithKline (GSK), Bristol-Myers Squibb (BMS), MSD and Johnson & Johnson are the most important companies. Gilead, the absolute anti-HIV hegemonic position, has a global market share of up to 163.02%

In 2019, half of the global antiviral drugs TOP 10 are Gilead’s anti-HIV products. With the listing of Truvada, Atripla, Complera, Stribild, Genvoya, Odefsey, Descovy and Biktarvy, it has seized a huge market share in the field of anti-HIV virus. In 2018, Gilead ’s HIV drug sales reached $ 14.6 billion, occupying nearly 43% of the market. In 2019, Gilead accounted for US $ 16.4 billion in HIV drug sales. Cocktail therapy generated huge profits to Gilead in the global HIV antiviral market, with 12.38% YOY%, accounting for more than 50% of the global anti-HIV / AIDS market.

Source: Company annual reports

Gilead has sprung up by focusing on the research and development of antiviral drugs, having a leading position in the antiviral field worldwide. From the beginning of the company to the present, the focus of the field has allowed Gilead to have extremely high R & D efficiency and sales efficiency, and also minimize operating costs.

Except its own R&D investment, M & A have also expanded the product pipeline for Gilead. The listing of Biktarvy and the cocktail therapy-based products have become the top priorities of the company’s product line today. When the major overseas pharmaceutical companies with multiple products mix cut down some product pipelines and want to concentrate on some fields, Gilead’s focus has promoted it one of the most successful companies among global pharmaceutical companies.

| Time | Target Company | Amount

(100 million dollars) |

Acquired drugs | Product field |

| 1999 | NeXstar Pharmaceuticals Inc. | 5.41 | AmBisome(Amphotericin B) | Antifungal infection |

| DaunoXome(Daunorubicin Citrate) | Anti-HIV | |||

| 2002 | Triangle Pharmaceuticals Inc. | 4.02 | Emtriva(Emtricitabine) | Anti-HIV |

2006 |

Myogen Inc. | 21.52 | Letairis (Ambrisentan) | Pulmonary hypertension |

| Corus Pharma Inc. | 3.65 | Cayston(Aztreonam Lysine) | Inhaled antibiotics | |

| Raylo Chemical | 1.33 | Active ingredient | ||

| 2009 | CV Therapeutics Inc. | 13.37 | Ranexa(Ranolazine) | Angina |

| Lexiscan(Regadenoson) | ||||

| 2010 | CG Pharmaceuticals | 1.2 | Entospletinib | Clinical Phase II |

| GS-9876 | Clinical Phase II | |||

| 2011 | Arresto Biosciences,Inc. | 2.25 | simtuzumab | Expiration |

| Calistoga Pharmaceuticals | 3.75 | Zydelig(Idelalisib) | Chronic lymphocytic leukemia(CLL) and lymphadenoma | |

| Pharmasset | 106.06 | Sovaldi(Sofosbuvir) | HCV | |

| Ledipasvir | HCV | |||

| Harvoni(Ledipasvir/Sofosbuvir) | HCV | |||

| 2013 | YM Biosciences | 5.1 | Momelotinib | Expiration |

| 2015 | Galapagos | 7.25 | Filgotinib | Rheumatoid arthritis(RA)、Crohn disease |

| Phenex Parmaceutical | 4.7 | PX-104 | Clinical Phase II | |

| Epitherapeutics | 0.65 | 基因转录表现遗传调控药物 | Pre-clinical Research | |

| 2016 | Nimbus Apollo Inc. | 4 | NDI-010976 | Clinical Phase I |

| 2017 | Kite Pharma | 119 | Yescarta | Diffuse large B cell lymphoma |

| Cell Design Labs | 5.67 | synNotchTM | CAR-T and TCR-T Cell Therapy Platform | |

| ThrottleTM |

Table: Gilead’s Mergers & Acquisitions Cases

Gilead’s Potential Competitors 英文report

Besides Gilead, GSK, Johnson & Johnson and MSD also develop anti-HIV drug. Among other competitors, GSK is a traditional strong competitors in the field of HIV drugs. In 2019, two anti-HIV drugs (GSK’s products) ranked in the top ten of antiviral drugs, which are Triumeq(ranked third) and Tivicay (ranked sixth) respectively. Namely, GSK is Gilead’s most important opponent in the HIV field and the products of Gilead and GSK differentiate in anti-HIV drugs market.

| Gilead | GSK | |

| Competitive

advantages |

The anti-HIV products of Gilead can effectively control the HIV virus, making it difficult to develop AIDS. The drugs enable AIDS, a fatal disease to turn to a controllable chronic disease. | |

| Drug competitive difference | TAF (Gilead’s new nucleoside reverse transcriptase inhibitor-TAF)

|

Tivicay (GSK’s integrase inhibitor) |

HIV drugs (2018 drug sales ranking) |

Rank 1: Genvoya (Gilead): $ 4.624 billion

Rank 3: Truvada (Gilead): $ 2.997 billion |

Rank 2: Triumeq (GSK): $ 3.511 billion

Rank 4: Tivicay (GSK): $ 2.18 billion |

| Specialization | Currently focusing on the development of TAF, Biktarvy, as a new generation of “cocktail therapy” anti-HIV / AIDS drug, has the effect of long-term relief of patients’ symptoms and reduction of HIV virus content in the body. According to the clinical phase III results, after 96 weeks of treatment, the treatment effect of the patients is not inferior to that of Abacavir / Dolutegravir / Lamivudine. Until now, There has been no treatment failure and drug resistance. | Focusing on the development and innovation of integrase inhibitors (INSTI). Studies have shown that medication regimens containing integrase inhibitors have better virus suppression effects, lower incidence of adverse reactions, and better tolerance of patients. In 2013, GSK’s Tivicay went public, whose sales soar at a rate of $ 400-500 million per year for three consecutive years. In the past few years, GSK’s compound preparation Juluca , currently the only two-drug compound preparation that does not contain nucleoside reverse transcriptase inhibitors ,was approved by the FDA for marketing. |

| Therapy | HIV patients only demand to take one pill per day | Slower than Gilead, HIV patients only demand to take two pill a day |

| Research & Development efficiency | High

Over the past decade, Gilead has launched 15 antiviral therapies. |

Slow

Only 5 combination therapies listed in 20 years |

Table: Gilead & GSK competitive position comparison

2020 Gilead Market Forecast

Based on the gradual increasing trend of the number of HIV carriers and HIV/AIDS patients and the better performance of Biktarvy sales, it is expected that the market share will rise to 55% and the total sales revenues of anti-HIV drug will exceed 24.8 billion dollars in 2020.

更多代写:Planning代考 线上考试作弊方法 Online Quiz 代考 怎么写conclusion 英文论文 pestle模型

合作平台:essay代写 论文代写 写手招聘 英国留学生代写