ECON 7780

Assignment 5

ECON代写 The spread between the yield on a five-year bond issued by a company and the yield on a similar risk-free bond is 80 basis points. Assuming a ···

19.10 ECON代写

The spread between the yield on a five-year bond issued by a company and the yield on a similar risk-free bond is 80 basis points. Assuming a recovery rate of 40%, estimate the average hazard rate per year over the five-year period. If the spread is 70 basis points for a three-year bond, what do your results indicate about the average hazard rate in years 4 and 5?

The average hazard rate per year over the five-year period is: 0.8%/(1-40%)=0.0133

The average hazard rate per year over the 3-year period is: 0.7%/(1-40%)=0.0117

The average hazard rate for year 4 and 5 is: (5*0.0133-3*0.0117)/2=0.0158

Thus, the average hazard rate in year 4 and 5 is 1.58%

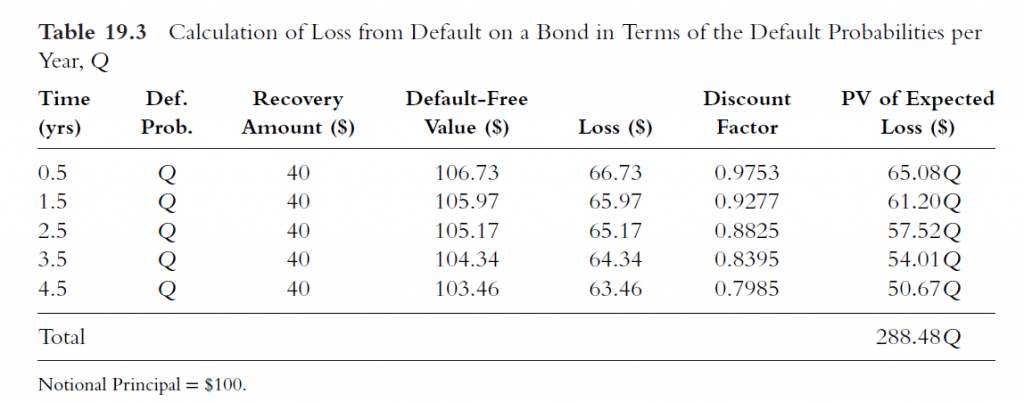

19.14 ECON代写

A four-year corporate bond provides a coupon of 4% per year payable semiannually and has a yield of 5% expressed with continuous compounding. The risk-free yield curve is flat at 3% with continuous compounding. Assume that defaults can take place at the end of each year (immediately before a coupon or

principal payment) and the recovery rate is 30%. Estimate the risk-neutral default probability on the assumption that it is the same each year using the approach in Table 19.3.

Answer: ECON代写

First, calculate the Price of corporate bond:

P1=2e-0.05*0.5+2e-0.05*1+2e-0.05*1.5+2e-0.05*2+2e-0.05*2.5+2e-0.05*3+2e-0.05*3.5+102e-0.05*4 =96.194

And with the similar equation we can found the price of risk free bond: P2=103.657

The expected loss from default should be =7.463

So the 272.929Q=7.463

Q=0.0273, the implied probability of default is 2.73% per year.

更多其他:代写作业 数学代写 物理代写 生物学代写 程序编程代写 Data Mining代写