Problem Set I

英国经济学assignment代写 Assume that there is no bank, nor investment opportunities. What is her optimal consumption and utility.

Question 1

Consider a two dates economy (t=0 and t=1) with certainty and where a consumer named Sophie has preferences over current and future consumption given by

U(c0,c1)=ln c0 + 0.9 ln c1,

Sophie has an initial endowment of 100 euros (at t=0), and she will receive her salary of 150 euros at t=1.

a) Assume that there is no bank, nor investment opportunities. What is her optimal consumption and utility.

b) Assume now that there is a bank offering r =4%, which is recently opened in her town. She can borrow and lend at the bank interest rate r without any transaction costs.

i.What is her optimal borrowing or lending?

ii.What is her optimal consumption? And, Does the bank make Sophie’s life better off?

iii.How does the optimal amount of borrowing/lending change as r changes? Interpret your results. 英国经济学assignment代写

c) Assume that her neighbors are trying to start up a factory. If she can invest 90 in this factory, then she will get 110 in t=1. The bank interest rate is 4%.

i.Should she invest into the factory?

ii.What is the maximum she can consume in each period if she invests into the factory.

iii. Find the optimal consumption and her utility assuming she accepts the project.

d) There is another investment opportunity that yields 150 in t=1. What is the maximum cost she is willing to pay for that project?

Question 2

You are requested to solve the exercise of section 2.5.2 with three dates that was left as an exercise.

More specifically:

Suppose that there are three dates – time 0, time 1 and time 2. The individual’s utility function is U(c0, c1, c2), with the usual assumptions concerning partial derivatives and concavity. Assume that the firm invests I# at date 0 and this yields Y01 = f01(I01) at time 1; it invests I12 at time 1 and this yields Y12 = f12(I12) at time 2. Firms can also invest at time 0 to have payoffs at time 2 given by Y02 = f02(I02) (long term investment). The individual borrows (or lends) L01 at date 0 to be repaid at date 1 at interest rate r01. He borrows L02 at date 0 to be repaid at date 2 at interest rate r02 per period. Finally, he borrows L02 at date 1 to be repaid at date 2 at interest rate r$’. The agent has endowments in every period: w0, w1 and w2.

a) Compute the first order conditions and relate them with the condition of no arbitrage.

b) Do you think Fisher separation and unanimity hold when agents have endowments in more than one period and there are many investment opportunities as here?

Question 3 英国经济学assignment代写

There are two firms in the economy who are 100% financed with equity. There are two possible states of the world in the future, State 1 occurs with probability 0.30, while State 2 occurs with probability 0.70. The following table summarizes the payoffs and prices of each firm:

a)Explain and document (compute the payoff matrix) whether markets are complete or not in the following alternative cases:

- Shares of both firm A and B are traded

- Only shares of firm A are traded

- Firm A issues debt with face value 30 and both the equity and the debt are traded

b)Find the prices of the Arrow securities in the first case (firms A and B are traded). What is the interest rate?

c)Now, suppose there are two investment projects in the economy with the following payoffs and prices.

Compute the expected net present value (ENPV) of each project. Which projects should firms undertake?

Question 4

Consider an economy with two dates, 0 and 1. At date 1 there are three states of nature. There are three securities, which are traded at time 0. Security X has payoffs (2, 3, 0) in the three states respectively; its price is 1.Security Y has payoffs (5, 2, 1) and a price of 2. Security has payoffs (1, 1, 1) and a price of 1.

a)How can elementary portfolios, i.e., Arrow securities (AS), be constructed? Describe the portfolio positions.

b) What is the price of each Arrow securities? What is the interest rate in this economy?

c)Use the prices of the Arrow securities to price the following assets:

i.A European call option on Security X with strike price K=1.

ii.A European put option on Security Y with strike price K = 3.

iii.Find the forward price of Security X using the cost of carry model.

iv.A bond with face value 5.

Question 5 英国经济学assignment代写

The current price of Meta Platforms, Inc. (formerly Facebook, Inc.) stock is $343 and its volatility is 20% per annum. There is a European option on Meta stock that has the strike price of $340 and expires in 3 months.

The risk-free interest rate is 3% per annum. All Black-Scholes assumptions hold.

a)Apply Black-Scholes formula:

a European put price with strike $340 expiring in 3 months, and a European call price with strike $340 expiring in 3 months.Does the put- call parity hold?

b) Given the Black-Scholes formula for a put option and put-call parity,derive the formula for a call option. 英国经济学assignment代写

c)Given the call price and the put price found in a), assume you discover a future contract with a forward price 344 expiring in 3 months. The contract size is 100 shares of Meta Platforms, Inc. The put and the call will also come with 100 shares. Determine if there is any arbitrage opportunity. If yes, then describe your arbitrage strategy.

Help: you can compute the values of the standard normal distribution by using the R function “pnorm()”

Question 6

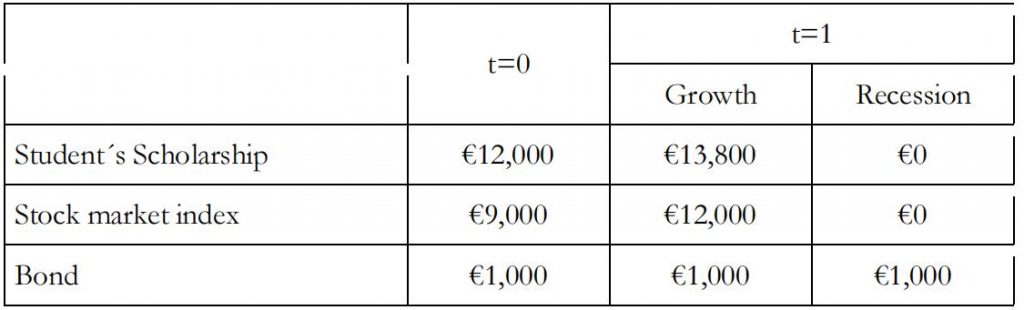

Consider a master Student currently (t=0) receiving a scholarship of €12,000. The economy can be either a boom or a bust, and his performance will be perfectly correlated with the economic states. In other words, the student will pass all the courses and receive a PhD offer with 15% growth in the scholarship in a boom.However, the student will fail some courses and lose the scholarship in a bust IBEX 35 (the benchmark stock market index of the Bolsa de Madrid) is available (Price=€9,000) in the country that will have a value of €12,000 in a boom and 0 otherwise. There is also a risk-free bond (RFB) with a price of €1000 at t=0 that gives a payoff of €1000 in each state in the future.

The following table summarizes the information:

Consider that this student can also trade a future contract on the stock market index, and both a put and a call with strike price €10,000 on the same index.

a.Find the prices of the futures and the options in the absence of arbitrage.

b.Assume that the student wants to consume the same amount today and in the future (regardless of the state).

i.Compute the portfolio of Arrow securities that allows him to meet his desires.

ii.Assume that the Arrow securities are not available. Is it possible for the student to smooth consumption trading the risk-free bond and the stock market index?

iii.Compute the student’s portfolio when he can only trade the futures and the call option.

iv.Compute the student’s portfolio when he can only trade the put and the call option.

Question 7 英国经济学assignment代写

Consider an economy with perfect and complete markets. It is a one-period economy with two dates (t=0,1) and uncertainty in period 1 is specified by the existence of states of nature s=1,2,….,S, (S>2). Consider an owner-manager of a firm who only consumes at t=0, so that his objective is to maximize the current value of his firm. There is only one consumption good in this economy. The firm’s earnings are zero at t=0 and Xs =s, s=1, 2,……,S at t=1. There is limited liability.

a.Interpret limited liability.

b.Assuming that there are no arbitrage opportunities in this economy, what is the best capital structure the manager can choose?. PROVE your assertion.

Question 8:

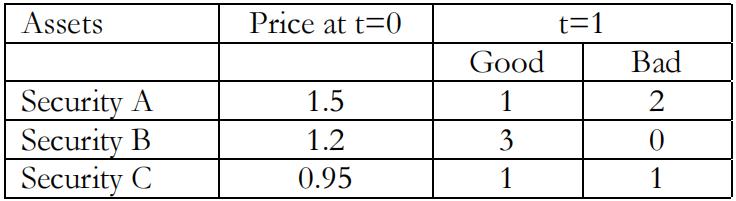

There is an economy with two dates t= 0,1 and two states at t=1 (good or bad). There are three assets in the economy characterized by the following prices and payoffs:

a.Are markets complete? Explain.

b.Price a European call option on Security A with strike price K=1.

i.by a replicating portfolio that only uses Security A and Security B;

ii.by a replicating portfolio that only uses Security B and Security C;

iii. would the option price be different if only securities A and C can be traded?

iv.Which assets are redundant in this economy?

更多代写:澳洲春季网课代上 gmat替考 澳大利亚数学代考价格 北美Essay代写收费 北美Business Plan代写 留学essay代做

合作平台:essay代写 论文代写 写手招聘 英国留学生代写