ECON 7780

Assignment 4

经济学作业代写 Suppose that we back-test a VaR model using 1,000 days of data. The VaR confidence level is 99% and we observe 17 exceptions. Should we reject···

12.9 经济学作业代写

Suppose that we back-test a VaR model using 1,000 days of data. The VaR confidence level is 99% and we observe 17 exceptions. Should we reject the model at the 5% confidence level? Use a one-tailed test.

In this case, to conduct the one tail test we use the excel to do it.

The probability of 17 or more exceptions is: 1- BINOMDIST(16,1000,0.01,TRUE)= 0.02639

So we can reject the model at the 5% confidence level obviously.

12.12 经济学作业代写

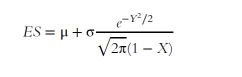

The change in the value of a portfolio in one month is normally distributed with a mean of zero and a standard deviation of $2 million. Calculate the VaR and ES for a confidence level of 98% and a time horizon of three months.

The SD in 3 months should be 2√T=2√3=3.464 million. And N-1(0.98)=2.054.

So the 98% 3-month VaR should be 3.464*2.054=7.11 million

The 98% ES (3 month) should be =8.39 million, according to the formula.

12.13 经济学作业代写

Suppose that each of two investments has a 4% chance of a loss of $10 million, a 2% chance of a loss of $1 million, and a 94% chance of a profit of $1 million. They are independent of each other.

(a) What is the VaR for one of the investments when the confidence level is 95%?

(b) What is the expected shortfall when the confidence level is 95%?

(c) What is the VaR for a portfolio consisting of the two investments when the confidence level is 95%?

(d) What is the expected shortfall for a portfolio consisting of the two investments when the confidence level is 95%?

(e) Show that, in this example, VaR does not satisfy the subadditivity condition, whereas expected shortfall does.

a). the VaR at 95th point should be 1 million. 经济学作业代写

b).the ES for the confidence level at 95% should be:

0.2*1+0.8*10=8.2 million for each of the investment

c).since they are independent to each other,

there is 0.04*0.04=0.0016=0.16% loss 20 million

and 0.04*0.02*2=0.16% loss 11 million

and 2*0.94*0.04=7.52% loss 9 million

and 0.02*0.02=0.0004=0.04% loss 2 million

and 2*0.02*0.94=3.76% loss 0 经济学作业代写

and 0.94*0.94=88.36% earn 2 million

so it’s obviously that the VaR at 95% is 9 million

- d) the ES at 95 % level should be

=(0.16/5)*20+(0.16/5)*11+(4.68/5)*9 = 9.416 million

- e)the subadditivity condition means that the risk for 2 portfolios after merged should be no longer than the sum of risk of each one before.

In this case, the VaR is 9 at 95 percent point which is larger than the sum of each one (1+1)

But the ES is satisfied with the condition, the ES at 95 percent point= 9.416 is smaller than the sum of each one (8.2+8.2).

更多其他:代写作业 数学代写 物理代写 生物学代写 程序编程代写 Python程序代写