MSFI 435 – Empirical Finance Fall 2020

Assignment 4 (Section I – Wednesdays)

实证金融作业代写 You proceed to contrast your colleague’s story against yours. You collect a random sample of 167 announcements of debt issuance.

Part I – Concepts 实证金融作业代写

1.You are interested in how investors react to announcement that a firm will issue new debt.Your colleague thinks that these events are uninformative—that they do not elicit any market reactions. You, on the other hand, believe that investors see debt issuance as good news, and thus reactions to this type of announcement should be positive. You think that way because debt is cheaper than equity, and the company may be in a better shape being funded by cheap capital.

You proceed to contrast your colleague’s story against yours.

You collect a random sample of 167 announcements of debt issuance. Each data point i in the sample is a firm F and a date t such that F announces on day t that it will issue new debt. Then, for each announcement, you compute the abnormal return, ARi, of the firm over the announcement day. Abnormal return is defined as firm return minus market return. Recall the notion of abnormal return: if nothing else is going on, the abnormal return should be equal to zero. Your analysis reveals that the average of the ARi measures over all data points was +1.03%, while the standard deviation of the AR measures was 7.30%. 实证金融作业代写

Use the data above to formally analyze your idea that such announcements are informative. Treat your colleague’s story as the null hypothesis and your story as the alternative hypothesis.

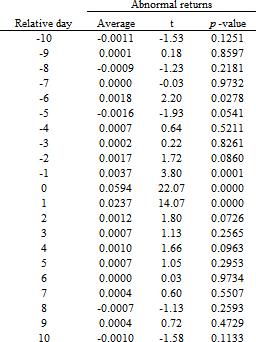

2.An event study of merger announcements tracks what happens to the targets’ returns aroundannouncement Merger announcements occur sometimes after the close of the market, so reactions to such announcements may take place in the next trading day.

The pattern is shown in the figure below. Take the first row of the table, for example: it states that average abnormal returns (where abnormal return is measured as the target’s stock return minus the market return) across targets for the 10th trading day preceding the merger announcement is –11 basis points, or –0.11%.

Figure 1: Targets’ abnormal returns around merger announcements

Discuss whether merger conveys good news, bad news or no news for the target. Then discuss whether markets are efficient in incorporating the information in the merger announcement.

Part II – Empirical Examination 实证金融作业代写

This part will empirically explore the reactions to two distinct, although related, events. They are both associated with the inclusion of firms in the S&P500 index. The first event uses as event date the day a firm is announced that it is going to be added to the index, and the second uses as event date the effective date of the inclusion in the index.

For each event, we want to examine two hypotheses. First, we want to check whether the announcement that a firm will be included in the S&P 500 carry any implication about the value of the firm.Our null hypothesis is that there is no valuation implication of being part of the index, so we write:

H0: No price reaction to the announcement of inclusion in the S&P 500

Ha: There is price reaction to the announcement

Our second hypothesis is conditional on the rejection of H0 . If we do find reactions to announcements of inclusion in the S&P 500 we want to further examine the efficiency of the market in impounding new information in the firm’s stock. 实证金融作业代写

For that, we look at the overall price pattern around (and more important, after) the event date.

We can also examine what happens with the price of stocks at the effective date of inclusion. Market efficiency would tell us that there should be no price response to that date, since it is completely predictable.

A hint about the results: It happens that firms do enjoy abnormal returns (that is, their values increase) once they are added to the index. That is, somehow the inclusion of the firm in the index, a decision that is outside the realm of the firm’s scope, is to be considered good news. The initial explanation for abnormal returns around the inclusion on the index had to do with price pressure from index funds, as these funds have to add a firm to their portfolio once the firm enters the S&P 500, but has since then evolved to many different reasons, e.g., improved liquidity, improved operating performance, and increased investor awareness. The main literature on the topic started with Shleifer (1986), “Do Demand Curves Slope Down?,” Journal of Finance 41 (available on Canvas), and was followed by a plethora of other papers.

1.I have collected for you a sample of inclusions in the S&P500 index between 1962 and 2000.

The file, ‘sp500_ev.sas7bdat’ (available on Canvas), contains the following variables: PERMNO (permno of the company), ANNDATE_SAS (the announcement date), and EFFDATE_SAS (the effective date of the inclusion in the S&P500). Get this dataset from Canvas into your SAS environment.

2.Download stock returns and market returns data. Use a period that encompasses all the dates in your input file, let’s say, between between January 1st, 1962 and Dec 31, 2001. This step mimics steps 6 and 7 of Assignment 3. In particular, recall that stock returns appear in the DSF dataset (located at ‘/wrds/crsp/sasdata/a_stock’), and market returns appear in the dataset DSIX (at‘/wrds/crsp/sasdata/a_indexes’).

Of course, you can optimize your data collection and collect returns only around the important dates (let’s say 50 days around ANNDATE_SAS and 50 days around EFFDATE_SAS). It is up to you. 实证金融作业代写

(Hint: You will have to download stock returns for the whole sample period, but you do not need to download returns for stocks that are not part of the sample of inclusions in the index. That is, since you need returns only for the included firms you will need to upload the inclusions file into the WRDS server. Use the PROC UPLOAD, which as the name implies does exactly the reverse of the PROC DOWNLOAD we already know. So you will need to run a code like this:

Important: to avoid rerunning the downloading of the data, a task that can be time consuming since it depends on the performance of the Unix server, create a code to run steps 1 and 2, and once you are done, start a new code for steps 3 and onwards.)

3.Now you have your event dates clearly defined. The first event is the announcement of inclusionin the S&P Compute average abnormal returns for the firms included in the index around these announcement dates. You should fill a table similar to the one shown below.

AR stands for market adjusted returns, that is, the abnormal return when we subtract VWRETD from the firm’s actual return (RET variable). Recall from our event study on earnings announcement that we used PROC MEANS to collect the t-statistic (t-stat in the table above) and the p-value for testing the hypothesis that abnormal return is equal to zero.

(This step is very similar to what we did in class for the event study on earnings announcement. That is, we need to match the datasets, then compute abnormal returns, then average the abnormal returns according to the nature of the subsample. Lavoisier once explained that “in Nature, nothing is lost, nothing is created, everything is transformed”. Accordingly, use the code we discussed in class as a starting point for your analysis.)

Figure 2: Summary statistics, abnormal returns

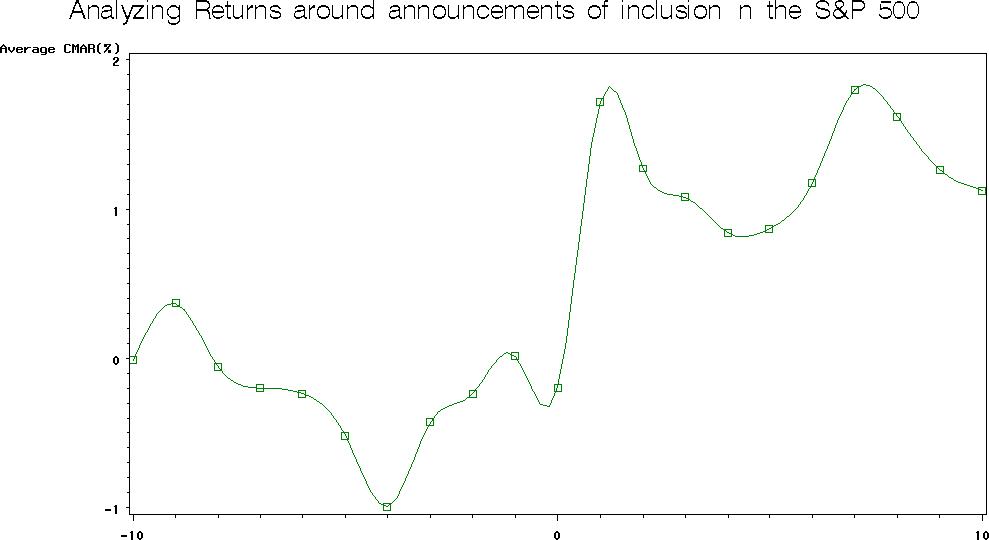

4.Plota graph of the cumulative abnormal return around the announcement Interpret your figure with the results you had for part 3).

Important: you are graphing cumulative abnormal returns, not market adjusted returns. A suggestion of the format of your graph (though not exactly its shape) is shown in Figure 3.

Figure 3: Average cumulative abnormal returns around event dates

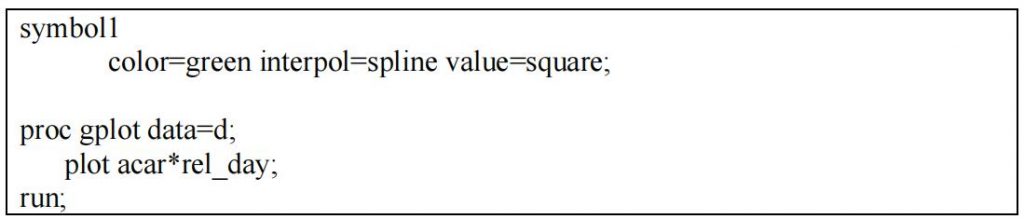

How to generate the graph? We’ve used the PROC GPLOT in class. Suppose you have a dataset D with the following variables: REL_DAY (from t=-10 to t=+10), ACAR (average cumulative abnormal return for that specific day and subsample). You thus write:

5.Now, repeat steps 3 and 4 using as the event date the date of the actual inclusion in the index (EFFDATE_SAS).

Given that many times a firm enters the index on the very same daytheannouncement of inclusion is done, and we want to separate the two events clearly, make sure you include here only firms for which the actual inclusion and the announcement are at least 4 days apart. That is, if D contains the data on inclusions, use a restriction:

6.Now, the important part: Interpret your results! Use the outputs from steps 3 through 5 to address the hypotheses in this study. Does an inclusion (both announcement and effective date) matter for firm valuation? Is the market efficient in dealing with this information? Make sure you state your hypotheses clearly, and formally examine them from a statistical standpoint.

更多代写:加拿大作业代做推荐 雅思代考 金融assignment代做 加州本科essay代写 加州大学music论文代写 代写为什么被发现

合作平台:essay代写 论文代写 写手招聘 英国留学生代写