Macroeconometrics 1: The Basic Building Blocks

(Graded Homework Problems)*

宏观计量经济学作业代写 This problem continues the one with the same background as in this Lesson‘s practice problems with solutions.

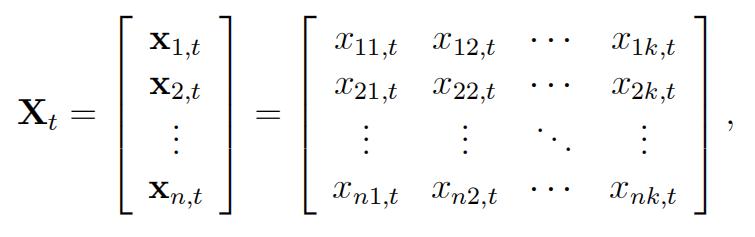

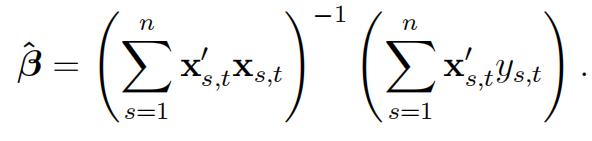

1.Let xs,tbe the 1 × k vector of explanatory variables for observation s such that 宏观计量经济学作业代写

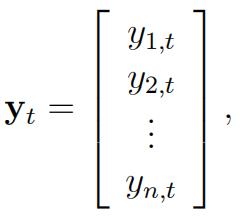

so that for ‹ = 1, …, n

xs,t = [ xs1,t xs2,t … xsk,t ],

and

where ‹ = 1, 2, …, n. Show that the OLS estimator β^ can be written as:

2. This problem continues the one with the same background as in this Lesson‘s practice problems with solutions. Let β^ be the OLS estimate from the regression of ¢t on yt. Let Xt be a k × k non-singular matrix and define: 宏观计量经济学作业代写

zs,t≡ xs,t At

for ‹ = 1, …, n. Therefore, xs,t is 1 × k and is a nonsingular linear combination of xs,t. Let Zt be the n × k matrix with rows xs,t. Let β˜ denote the OLS estimate

These lecture notes closely and sometimes literally follow sections from: Dowling, Edward T. Intvo− ductson to Mathematsca1 Economscs. Shaum‘s Outlines, 3rd ed., McGraw Hill, 2001 Nicholson, Walter. Mscvoeconomsc fheov4: Bassc Pvsncsp1es and Estenssons. South-Western College Pub, 9th ed., £OO4¡ Simon, Carl P., and Lawrence Blume. Mathematscs fov Economssts. New York: Norton, fi994¡ Sydsaeter, Knut, and Peter J. Hammond. Mathematscs fov Economsc Ana14sss. Prentice Hall, 1995.

from a regression of yt on Zt. Show that the estimated variance matrix for β˜ is ![]()

3.Thisproblem continues the preceding one as well as the one with the same background as in this Lesson‘s practice problems with solutions. Let β^ be the OLS estimate from the regression of ¢t on Xt. Let At be a h × h non-singular matrix and define:

zs,t≡ xs,tAt

for s = 1, …, n. Therefore, xs,t is fi × h and is a nonsingular linear combination of xs,t.

Let Zt be the n × h matrix with rows xs,t. Let β˜ denote the OLS estimate from a regression of yt on Zt. Let βˆj be the OLS estimates from a regression of yt on:

1, x2,t, …, xk,t

and, let β˜j be the OLS estimates from a regression of yt on:

1, a2x2,t, …, akxk,t,

where the as are constants and aj ƒ= 0 for j = X, …, h. State the mathematical rela- tionship between β˜j and βˆj .

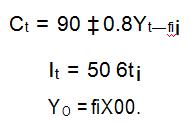

4.Consider the following lagged income determination model: 宏观计量经济学作业代写

In equilibrium, Yt = Ct ‡ It akin to the development in this Lesson‘s practice problems with solutions.

(a)Find the time path of national incomeYt.

(b)Characterize the stability of the time path obtained in part(a).

更多代写:墨尔本代写assignment GRE代考 book review代写 写essay 代写毕业论文 美国代写被抓

合作平台:essay代写 论文代写 写手招聘 英国留学生代写