Assigment4

加拿大经济学代写 Let utdenote the residuals from the long-run relationship. Use these residuals to perform the Engle-Granger test for cointegration.

1.The file COINT XLS contains monthly values of the Japanese, Canadian and Swiss consumer price levels and the bilateral exchange rates with the United States. The file also contains the U.S. consumer price level. 加拿大经济学代写

The names on the individual series should be self-evident. For example, JAPANCPI is the Japanese price level and JAPANEX is the bilateral Japanese/U.S. exchange rate. The starting date for all vari- ables is January 1974 while the availability of the variables is such that most near the endof 2013. The price indices have been normalized to equal 100 in January 1973 and only the U.S. price index is seasonally adjusted.

(a)Form the log of each variable and pretest each for a unit root. Can the null hy- pothesis of a unit root be rejected for any of the series? How might you proceed ifyou found that the S. CPI was trend stationary?

(b)Form the log of each variable. Estimate the long-run relationship between Japan the U.S.as

i.Do the point estimates of the slope coefficients seem to be consistent with long-runPPP? 加拿大经济学代写

ii.From the t-statistics, can you conclude that the Japanese CPI is not signifi- cant at the 5%level?

(c)Let utdenote the residuals from the long-run relationship. Use these residuals to perform the Engle-Granger test for cointegration. If you use eleven lagged changes, you should find

- The t-statistic on the coefficient for ut—1 is 3.44. From Table C, with three variables and 457 usable observations, the 5% and 10% critical values are about 3.760 and 3.464, respectively. Do you conclude that long-run PPP fails?

(d)Repeat parts (i) and (ii) using Canada and Switzerland. If you use the residuals from the long-run equilibrium relationships you shouldfind 加拿大经济学代写

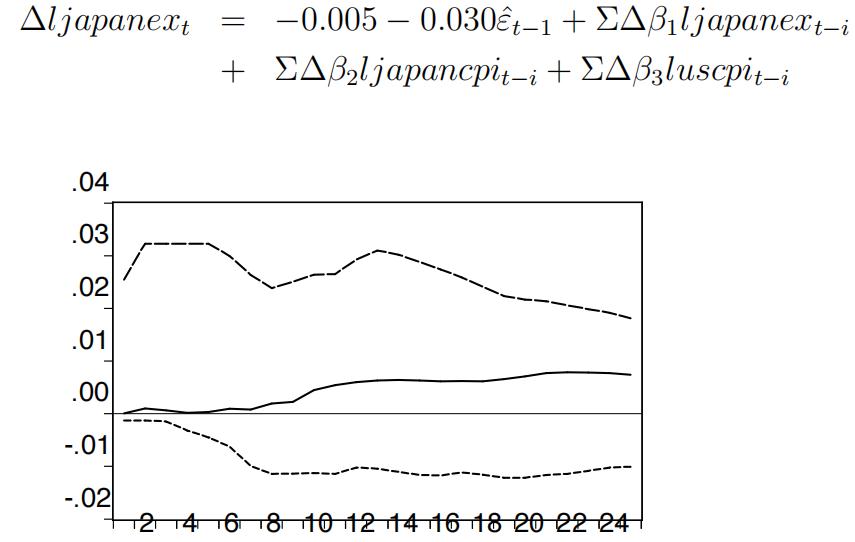

(e)Although (at conventional significance levels) we reject the null hypothesis of long-run PPP between Japan and the United States, estimate the error-correction model for ljapanext. If you use 11 lagged changes of each variable, you should find

Figure 1: (solid) U.S. Price Shock, (short dash) Japanese Price Shock, (long dash) Ex Rate Shock

where ![]() is the residual from the equilibrium relationship above and eleven lagged changes are used for each variable. The t-statistic on the error cor- rection term is 3.54. Which of the variable(s) can be said to be weakly exogenous? 加拿大经济学代写

is the residual from the equilibrium relationship above and eleven lagged changes are used for each variable. The t-statistic on the error cor- rection term is 3.54. Which of the variable(s) can be said to be weakly exogenous? 加拿大经济学代写

(f)Obtainthe impulse response functions using the ordering uscpit ! ljapancpit ! ljapanext. As in Figure above, you should find that the U.S. price shock has little e↵ect on the exchange rate but that the shock to the Japanese price level causes the yen to The response of the exchange rate to its own shock is immediate and permanent.

(g)Are the results of the cointegration test sensitive to the normalization (i.e. which of the variables is used as the ’dependent’ variable) used in the equilibrium re- gression?

2.In the previous question, you were asked to use the Engle-Granger procedure test for PPPamong the variables log(canex), log(cancpi), and log(uscpi). 加拿大经济学代写

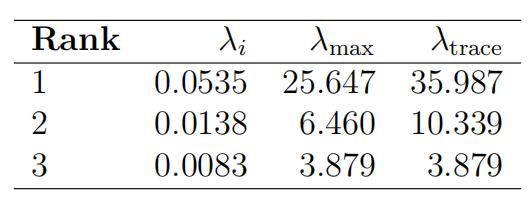

(a)Nowuse the Johansen methodology and constrain the constant to the cointegreat- ing vector to obtain:

- Usethe table to show that there is a cointegrating vector.

(b)Consider the estimated cointegratingvector:

−0.949 log(canex) − 6.484 log(cancpi) + 1.600 log(uscpi) + 31.653 = 0

- Normalize with respect to the exchange rate. Does the long-run relationship seem to be consistent with PPP?

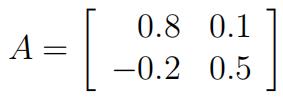

6.An econometrician estimates a vector autoregression for two variables x and y using onelag of each The estimated VAR is 加拿大经济学代写

The variance covariance matrix of the shocks et and ut is known to be diagonal.

(a)Write a computer program to, compute the impulse response functions out toten periods for a shock to εt, as well as et. (Hint: Simulate the following difference equation)

where

(b)Plot the four impulse response functions for t = 1, . . . ,10.

更多代写:网课代考会计 托福代考被抓 物理Final exam代考 文科艺术essay代写 温哥华essay论文代写 apa怎么写

合作平台:essay代写 论文代写 写手招聘 英国留学生代写