Macroeconometrics 7: Advanced Multivariate TimeSeries (Graded HW Problems)

代做Macroeconometrics There is no need for you to try multiple specifications nor justify why you chose a particular type of version of the data to model.

1.The dataset HW6.dta contains the following data: 代做Macroeconometrics

apl (the average product of labor in the US); u (the level of unemployment in the US); lf (the level of the labor force in the US); v (the level of vacancies in the US); and quarter (a time variable). Create a.do file called HW7Control.do that models vacancies and unemployment as a recursive VAR. You are free to use whatever version of the data you like: levels, log levels,growth rates, etc. There is no need for you to try multiple specifications nor justify why you chose a particular type of version of the data to model.

Just make sure that all your iís are dotted and all your t’s are crossed, by which I mean that you should carefully follow the procedures gone over in the last two Lessons to model VARs. In addition, you should thoroughly annotate your code explaining your reasoning behind any one procedure that you implement and your results. Finally, please have your code generate in a single graph the 4 possible orthogonalized impulse response functions that will emerge from your modeling and annotate in your code your interpretation of these results.

2.The dataset conwages.dta corresponds to the wages example in the textbook’s chapter on nonstationary time series.

Use this dataset to model wages as a VECM per the prompts in this textbook’s chapter and this Lessonís lecture notes making sure to follow the ‘5 stepsînoted in both reading materials. Your model should be developed in a Stata .do file called ConwagesControl.do. Large portions of this exercise are already solved for you in the textbook. 代做Macroeconometrics

However, the idea behind this exercise is that by now you should have enough knowledge on Macroeconometrics that you should be able to process the information in the textbook and explain the material to me as if I were your student. So, I will ask that you please thoroughly annotate your code as if it were meant for teaching someone else how to go about modeling a VECM. This will require going beyond the textbook’s development. In particular, please relate your results to problem 5 from this Lesson’s practice problems with solutions. I.e., explain to your ‘student’ how Stata output corresponds to the background theory. For this problem, in addition to the textbook and this Lesson’s lecture notes, you will find the following two Stata webpage resources very helpful:

(a) https://www.stata.com/manuals13/tsvecintro.pdf

(b) https://www.stata.com/manuals13/tsvec.pdf#tsvec

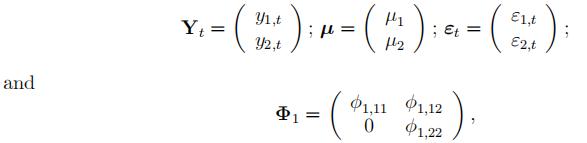

3.Consider a VAR with two variables: y1,tand y2,t. In particular, assume 代做Macroeconometrics

where εt is white noise and the μs and Ø s are parameters. Assume that the VAR is stable and that the system begins in steady state. Then, in period 0, y2 is pushed out of steady state given a non-orthogonalized one-time one-unit shock to ε2. Amid this backdrop, what is the period-2 non-orthogonalized impulse response function for y1 equal to (in response to the shock to ε2)? Please show your work and explain your reasoning with careful detail. Also, the impulse response function should be stated explicitly in terms of parameters, only.

更多代写:北美Geography代写 pte代考 澳大利亚会计写代写 本科essay代写 北美留学生论文代写范文 poster是什么

合作平台:essay代写 论文代写 写手招聘 英国留学生代写